The Catalyst: A Systemic Supply Shock

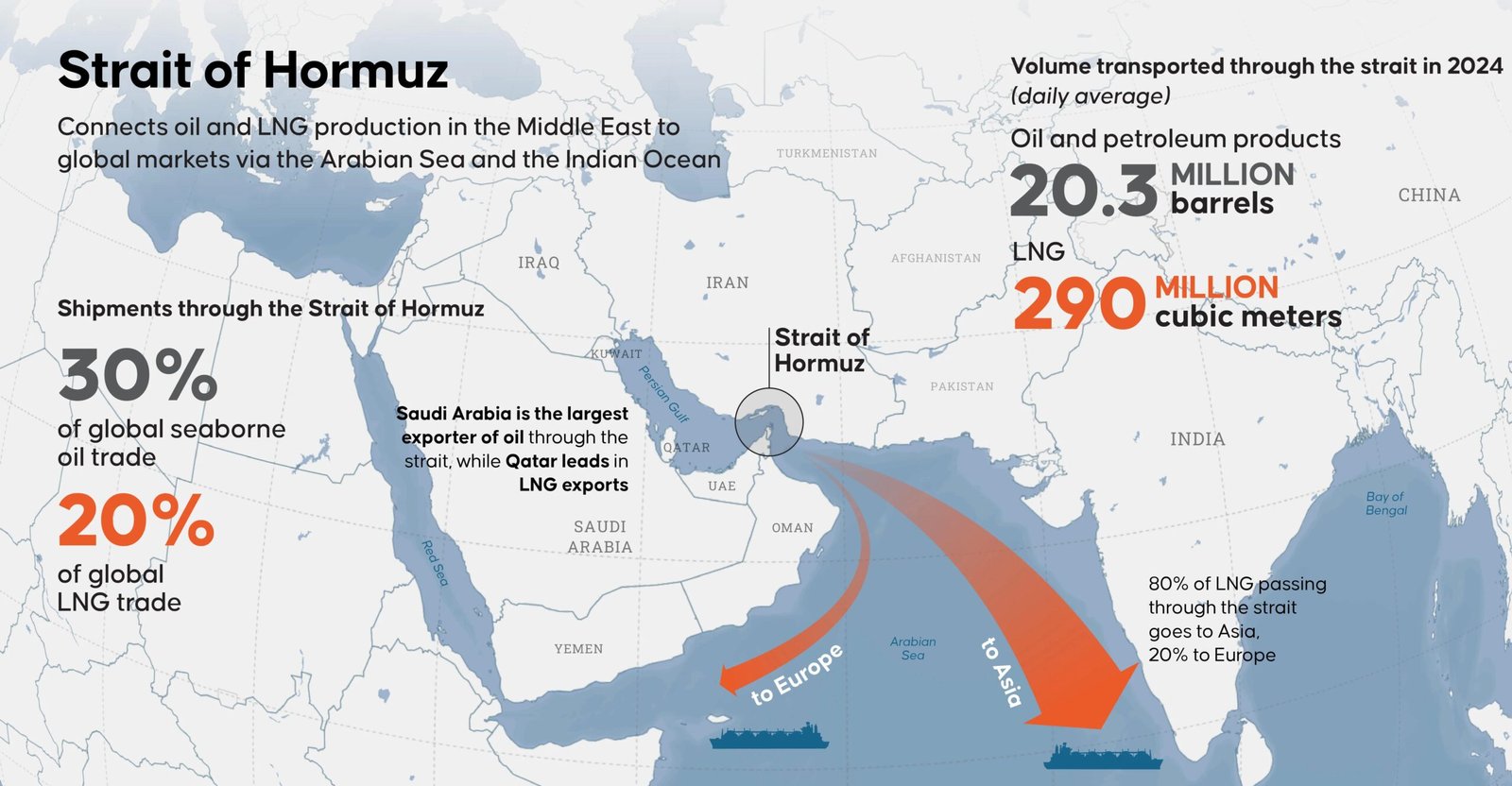

The immediate catalyst for Europe’s scramble was an Iranian strike on Qatar’s Ras Laffan facility, the world’s largest LNG hub, which caused significant damage and severely disrupted supplies. Consequently, European gas prices surged by 35%, and tanker traffic through the Strait of Hormuz plummeted amid escalating security threats. The closure of the strait has caused Gulf producers to curtail output by millions of barrels daily, leading experts to project that oil prices could exceed $100 per barrel. French President Emmanuel Macron condemned the attacks as a “reckless escalation,” warning that the destruction of energy production capacities will leave a lasting impact on global markets.

Algeria’s Strategic Pipeline Advantage

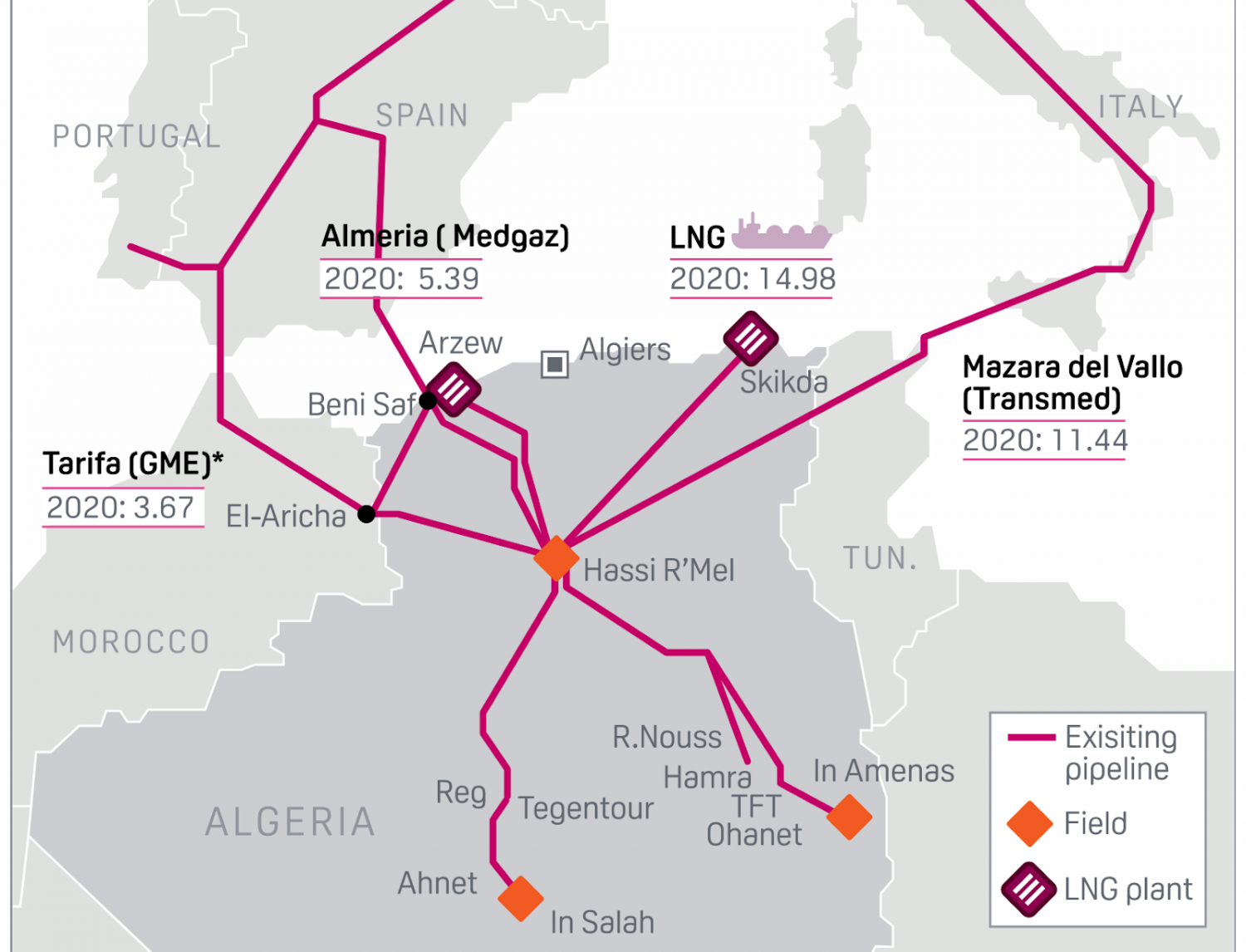

Unlike Middle Eastern suppliers that rely heavily on vulnerable maritime routes, Algeria benefits from direct pipeline connections to Europe. The country primarily supplies its northern neighbors through the TransMed pipeline to Italy and the Medgaz pipeline to Spain. This infrastructure effectively insulates Algerian gas exports from maritime chokepoints like Hormuz, cementing its reputation as a reliable, short-haul supplier during geopolitical crises.

The pivot is already yielding results; in January, Algerian pipeline deliveries to the European Union rose by 22% compared to the previous month. Furthermore, the global oil price spikes have indirectly benefited Algeria’s fiscal position, as higher prices increase the country’s export revenues from its oil sector.

Italy and Spain Accelerate Diplomatic Engagement

European nations uniquely exposed to the Qatari LNG disruptions have swiftly turned to Algiers to secure their grids.

Italy, which already sources around 30% of its gas from Algeria (totaling roughly 20 billion cubic metres in 2024), is actively seeking to expand deliveries. During a recent diplomatic visit to Algiers, Italian Prime Minister Giorgia Meloni announced an agreement to strengthen cooperation through their respective national companies, Eni and Sonatrach. Meloni emphasized that exploring new areas such as offshore projects and shale gas will help boost long-term gas flows from Algeria to Italy.

Similarly, Spain is in advanced negotiations to increase gas supplies through the Medgaz pipeline. Algerian gas already accounted for more than 29% of Spain’s imports in the first two months of the year. Spanish Foreign Minister José Manuel Albares confirmed ongoing discussions to potentially boost Medgaz flows by up to 10%, utilizing the pipeline’s roughly 1 billion cubic metres of annual spare capacity. Commercial ties remain deeply entrenched, with Spanish utility Naturgy holding long-term contracts for around 5 billion cubic metres of gas annually with Sonatrach.

Structural Constraints and Expert Perspectives

Despite the increased European demand, experts caution that Algeria cannot act as a silver bullet to fully replace the lost Gulf supplies. Analysts note that Algeria currently produces only about half the volume of LNG that Qatar does, and significantly expanding production capacities will require considerable time. Theresa Fallon, director of the Centre for Russia Europe Asia Studies, stressed that the economic effects of this disruption “will likely be felt for years”.

Algeria’s ability to capitalize on the crisis is hampered by internal constraints, including aging fields and infrastructure, rising domestic energy consumption, and a lack of recent upstream investment. Consequently, experts suggest that Algeria can only achieve modest, incremental output increases rather than transformative supply growth in the short term. Analysts also point out that attacks on major energy hubs mean that any short-term export increases from Algeria will only ease immediate pressure, but cannot completely offset the profound disruptions to global supply.

Looking Ahead

The closure of the Strait of Hormuz has starkly exposed Europe’s vulnerability to external shocks and elevated Algeria’s strategic importance within EU energy security planning. Thanks to its geographic proximity and robust pipeline infrastructure, Algeria serves as a vital stabilizer in an otherwise volatile market. However, inherent structural constraints dictate that Algeria can mitigate, but not entirely resolve, Europe’s energy deficit. Ultimately, the crisis reinforces a broader reality: energy security in the 21st century relies not on a single supplier, but on rigorous diversification, resilience, and a reduction in reliance on vulnerable maritime chokepoints.