The Empirical Anatomy of a Maritime Titan

The quantitative footprint of the Greek shipping sector is historically unprecedented and actively expanding. Between 2015 and February 2025, the capacity of the Greek fleet surged by more than 42%.

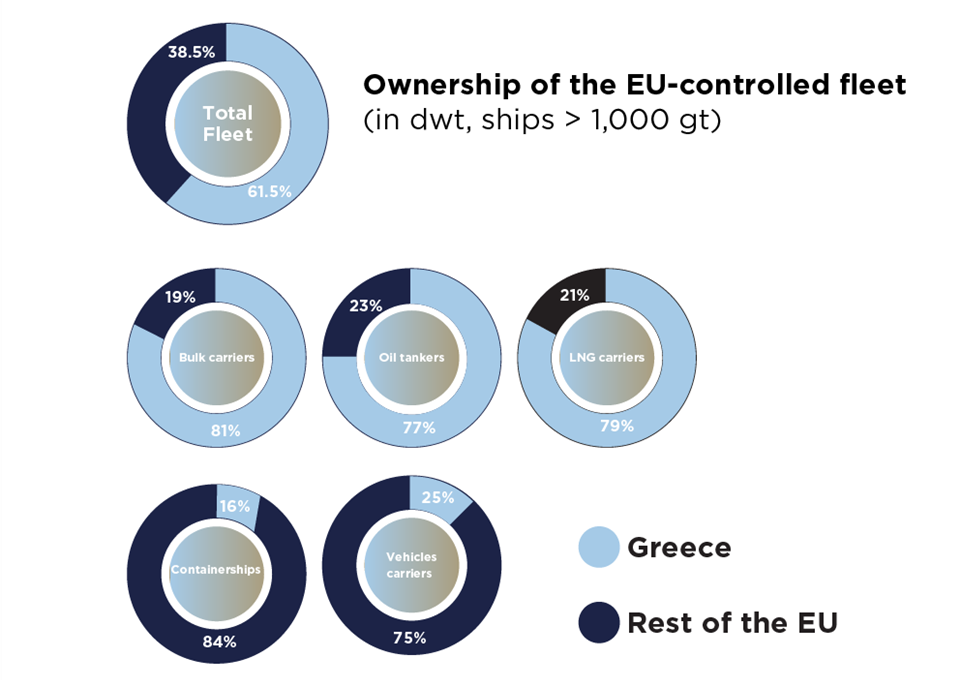

- Fleet Scale: Recent industry reports classify the Greek-owned fleet at 5,691 ships, representing the largest national fleet in the world and comprising 61% of the entire European Union merchant fleet. When evaluating strictly ocean-going vessels over 1,000 gross tons (GT), Greek owners control between 4,388 and nearly 5,800 vessels, with a collective carrying capacity ranging from 360.6 million to over 458 million deadweight tons (DWT) depending on the tracking index.

- Corporate Density: The industry is supported by a robust corporate infrastructure, with 78 independent Greek companies operating fleets that exceed 1 million DWT. Furthermore, over 20 Greek shipping companies are publicly listed on foreign capital markets, holding a combined market capitalization of more than $9 billion.

- Strategic Diversification: Greek shipowners deliberately avoid overexposure to a single market segment, maintaining top-tier global positions across multiple vessel classes. They control approximately 31% of the global oil tanker fleet, 25% of the world’s dry bulk capacity (transporting iron ore, coal, and grain), and roughly 22–23% of the liquefied natural gas (LNG) carrier market.

The Economic Engine: Domestic Impact and Global Reach

While the ships traverse the globe, the economic dividends are deeply felt within Greece. The maritime sector serves as the country’s largest economic engine by global revenue, generating an estimated $40 billion in annual gross revenues from charter rates and freight operations.

Domestically, the shipping cluster contributes between 7% and 8% of Greece’s total GDP, injecting approximately $14 billion in direct domestic value. It is responsible for 6% of private-sector employment, supporting between 150,000 and 200,000 high-paying jobs. This workforce spans direct seafaring roles—including the employment of over 200,000 foreign seafarers globally—and an extensive onshore ecosystem of shipyards, legal firms, brokerages, and financial institutions.

On a global scale, the fleet’s reach is unparalleled. In 2023 alone, Greek-controlled vessels executed over 160,000 port calls across 174 countries. Crucially, the fleet is a vital pillar of European energy security; analysis indicates that 40% of all crude oil imported to Europe by sea is transported via Greek tankers.

The DNA of Hellenic Success: Structure and Strategy

The enduring success of the Greek maritime sector is underpinned by unique operational philosophies and supportive institutional frameworks.

- Agile, Family-Owned Leadership: Unlike massive, bureaucratically heavy maritime corporations found elsewhere, Greek shipping firms are predominantly small-to-medium-sized family businesses. The owner is frequently the CEO, allowing for rapid, autonomous decision-making with minimal red tape.

- Mastery of the “Tramp” Trade: The majority of Greek operators specialize in the “tramp” or commodity trade. Rather than running fixed routes on set schedules, these vessels act as flexible assets, quickly repositioning to seize emerging, short-notice opportunities across varied customer needs.

- Counter-Cyclical Entrepreneurship: Greek shipowners are characterized by a risk-tolerant, entrepreneurial mindset. They routinely execute counter-cyclical investment strategies—acquiring new ships heavily during economic downturns when asset prices are low, and selling them for massive profits during market upswings. This aggressiveness is evidenced by Greece holding the third spot in the global order book for bulkers and tankers for 2023 and 2024.

- Institutional Ecosystems: The Greek government has actively fostered this growth. Notably, Law 89/1967 allows foreign companies to establish offices in Greece without incorporating under Greek law, providing tax benefits that have spurred massive growth in domestic ship management. Additionally, organizations like the Union of Greek Shipowners (UGS) facilitate a highly collaborative community where firms share data and form procurement alliances to leverage joint buying power for fuel and supplies.

Navigating 21st-Century Headwinds

Despite its monumental strength, the Greek shipping industry faces severe contemporary challenges. Melina Travlos, president of the UGS, recently highlighted that the industry is operating amidst profound economic, environmental, and geopolitical uncertainty, specifically pointing to ongoing threats to the freedom of navigation.

- Geopolitical Volatility: Security threats in critical maritime chokepoints, notably the Black Sea and the Strait of Hormuz, have forced Greek operators to continually reassess operational routes, resulting in drastically higher insurance premiums and logistical complexities.

- Regulatory and Environmental Pressures: Tightening international regulations, such as the IMO 2020 sulfur emission standards and future decarbonization mandates, demand massive capital expenditures. Greek owners are combating this through aggressive fleet modernization, investing in newbuilds equipped with digital optimization tools and testing alternative fuels like LNG, ammonia, and hydrogen.

Flag Registration Flight: Driven by the pursuit of cost efficiencies, regulatory arbitrage, and fierce global competition, a significant portion of the Greek-owned fleet is registered under foreign flags, including Liberia, Panama, and the Marshall Islands.

Charting the Future: Untapped Avenues for Growth

To future-proof its dominance, industry analysts suggest that Greece must expand beyond pure asset ownership and capture adjacent maritime markets:

- Third-Party Ship Management: While Athens is the world’s largest ship management hub—controlling over 5,000 deep-sea vessels—roughly 90% of these ships are Greek-owned. This leaves a massive untapped market for managing foreign-owned vessels. By comparison, over 70% of the vessels managed out of rival hubs like Singapore and Hong Kong are of foreign origin.

- Maritime Technology: Technological advancement in ship design, repair, and routing is accelerating, yet only about 2% of global maritime tech startups are founded in Greece. Given the nation’s deep maritime expertise, leaning into venture capital funding for patentable nautical technology represents a highly lucrative frontier.

- Shipyard Revitalization: Increasing domestic shipyard capacity would allow Greece to capture a much larger share of the highly profitable dry-docking and repair market for vessels transiting the Mediterranean Sea.

By leveraging its century-old heritage, maintaining its operational agility, and aggressively investing in green technology and digital integration, the Greek maritime sector is strategically positioned to remain the indispensable engine of global trade for decades to come.